Van-centric introduction!

We normally try to touch on a wider topic, or something of specific interest in these introductions, but with September being the busiest month in the year for registrations (the data for which is not available at time of writing), and with LCVs making up by far the largest share of the vehicles that XBG remarket, we can’t ignore what is going on in the new vehicle marketplace.

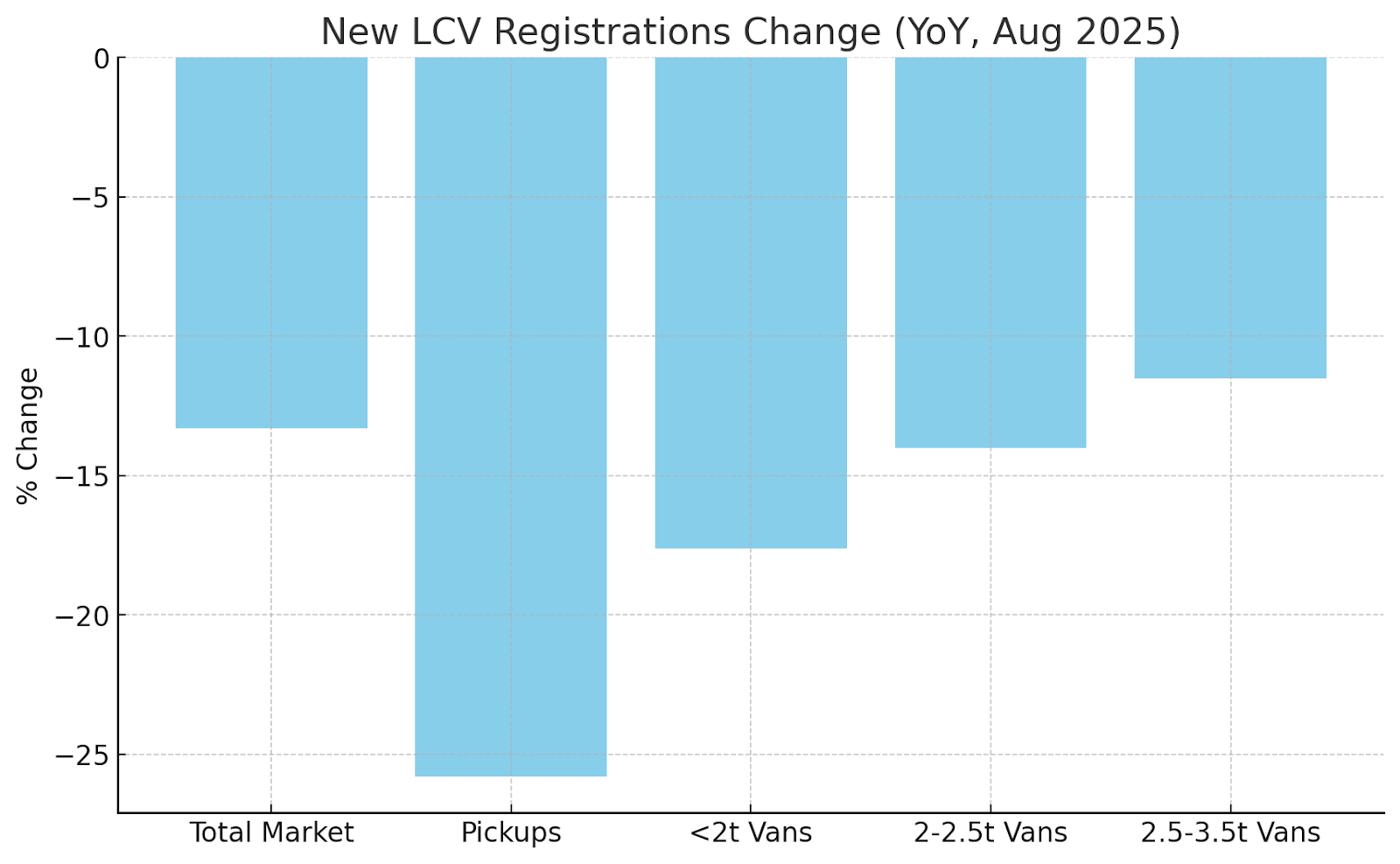

Monthly registrations have seen a ninth consecutive monthly year on year drop, with August registrations down by 13.3%, and overall registrations year to date down by 11.4%. While this might not seem significant to the untrained eye, it’s worth considering that continual growth in the use of LCVs in the UK has long been predicted due to more home deliveries, the increase in self-employment, and the popularity of lifestyle versions which double up as weekend family transport, and a working vehicle in the week.

So, what’s happening? Well, as usual, it is a combination of things. Undoubtedly the change in BIK rules on double cab pick-ups has taken the wind out of the sales in this area, with August registrations down by over 25%. This may well decline further still with many older new vehicle orders still being fulfilled.

Another factor is the 2025 ZEV mandate target of 16% leading to many manufacturers stipulating that fleet buyers take increasing proportions of BEV units to get the discount terms they need to balance their books. This is leading to a stand-off in many circumstances where the fleet buyer concerned has little desire to take on BEV units.

And, of course, there is the economy. Lack of growth and increasing costs are undoubtedly putting pressure on balance sheets, and putting off vehicle replacements is an easy win in reducing expenditure, especially when the difficult transition from Diesel to Electric propulsion is large in the mind of virtually every Fleet Manager.

New BEV LCV market

Yet again, we need to touch on this as it is certainly the most talked about area of business in many of our customer meetings.

While the ZEV mandate target for 2025 is 16%, overall, BEV LCV sales grew to 13% in August. By range, the Ford E-Transit Custom accounted for 19.4% of all registrations. The VW.ID Buzz Cargo was second with 14.9%, and the Mercedes-Benz e-Sprinter was third with 12.8%. The Ford E-Transit came fourth with a 9.8% share, and the Vauxhall Vivaro was fifth with 6.8%.

Even this moderate growth is somewhat forced of course, with manufacturers becoming exceptionally keen for the hard-working utility fleets to accelerate their change cycles and move over to BEV, while the other area of bulk registrations, short and medium-term rental businesses, continue to resist the transition due to lack of customer interest and high holding costs.

There is also a ‘watch-out here’ on residual values. Many of these are based on current used vehicle performance with a factor built in for ageing out of a model. And while most observers would say that used electric vans in the current market look pretty cheap already, this is with them making up less than 5% of the used market. As volumes increase over time it would seem logical that values decrease accordingly.

With all of this in mind the currently top-selling BEV LCV, the Transit E-Custom, seems to have an optimistic Residual Value position in most cases.

And with average holding terms extending out these days, there could easily be a glut of these in the market at 5-7 years old, all struggling to get anywhere near their residual values.

Used LCV Market

A relatively easy area for commentary this month. While Retail demand is steady in the lower price ranges, the overall Retail market is sluggish. Usually this would translate into poor auction performance, but observations are that most LCVs are selling very well indeed.

Auction yards are visibly much clearer of stock, with a relative shortage in most locations being seen right through September. Even with September new vehicle registrations usually producing part exchanges and de-fleets, auction volumes are not predicted to be strong for the foreseeable future. This sits well with the stock that is available which should continue to achieve good results as we move into autumn.

One of the highlights of September has been some batches of exceptionally well-maintained Ford Customs from one customer. Although the body condition was good, the critical aspect was the comprehensive service history with very regular servicing, and the vans being earlier non wet-belt versions. These outperformed guide values by over 40% in most cases.

Higher value Double Cab pick-ups continue to come under price pressure as the BIK changes are now more widely understood by the Trade. Sub £10000 examples and utility specifications don’t seem to be affected.

Lower mileage Luton and Low Loading body vehicles are in high demand, possibly because the rental companies generally don’t buy and churn this stock very often now. These can make astonishing figures against guide values, but then when list price and availability is taken into account, they look more sensible.

In summing up, the LCV market remains resilient, and largely in a good place, with the outlook for the latter part of the year showing no signs of immediate change.

Used Car Market

Signs that a market is weakening usually comes in the form of a marked parting of ways between desirable and the less desirable vehicles. This may be due to provenance, colour, specification, or mileage. This certainly seems to be the case in the used car market where anything but the most desirable examples are getting left behind by buyers in recent days.

There are some bright spots in the sub £10000 marketplace, and these ‘price range’ cars seem to be holding up as often happens when things get tougher.

One other very positive and interesting change is a continued pick up in the demand for used electric cars. These have looked great value for some time now and it seems the public are starting to latch on to this. CAP values increased over the August month end on many models, and although this surge in interest is never going to be strong enough to stem some of the heavy losses being felt by first owner funders, it is at least going to create more confidence for sale of the ever-increasing numbers coming off of fleet use.

Trucks and Trailers

Following a reasonable month of trading in July, August did turn out to be a fairly quiet affair in the used truck and trailer markets. Volumes of fresh stock arriving at auction during this month was also quiet, save for some Dropside trucks from a bottled gas supplier that were actually well received and sold well.

So, stability is the situation we find this month for trucks, with enough volume to satisfy the trade demands in most sectors.

Boxes are around in the usual volumes, with many of them being fridge boxes and, most of them being on DAF or Iveco chassis. As such only the very cleanest lower mileage examples are making the strongest money, with poorer trucks selling a fair way behind the ‘Book’ values.

Tractor unit prices remain stable this month with no real change in the outlook, the better specified 6×2 trucks with sleeper cabs are going to sell for the strongest money and within a reasonable time frame. But ‘poverty spec’ former supermarket examples remain available in volume and struggle to find buyers. DAF again form the vast majority of units available.

Tippers and Dropsides remain quite popular regardless of chassis, with a few newer ‘tridems’ appearing as used examples. On a tipper chassis these trucks are very popular indeed and making very strong money, with plenty of competition in the auction room. Dropsides are also selling well, especially if equipped with a crane behind the cab.

Trucks in this sector rely to an extent on ‘national infrastructure projects’; with some investment from Government currently, construction trucks and plant are enjoying some popularity.

Specialist trucks remain quite rare in the used markets and so, when they do appear always sell for strong money particularly if they are Euro 6. But even pre-Euro 6 examples are selling, mainly for export. Beavertails, mixers, recovery and tankers all fall into this category.

There remain plenty of trailers around, but demand is also quite healthy, so no real price surprises here this month. This double deck fridge seen at auction during the month sold extremely well to bidders both online and in the hall.

Plant and Equipment

After a relatively quiet August, sales in the plant and equipment sector started to pick up towards the end of the month, suggesting a strong September. With a lack of some buyers during this month though, prices of some more standard plant were down a little but the more specialist stock continued to sell well, mostly for export.

Agricultural sales were also a little slower this month as they usually are, with many farmers concentrating on harvest rather than investing in stock.

That said the example seen below, YL19KOB sold at Shoreham Vehicle Auctions for CAP money; with a warranted 54000 miles this attracted the trade buyers.

From the Rostrum

The view from the rostrum in August was actually very good, with LCV sales being described by our Auction manager as “on fire”! The direct from fleet stock has proved immensely popular at auction right through to the last week of August which was noticeably quieter. For cars it was a similar story, especially for ICE cars under £10k and BEV’s under £20k (retail). The more expensive the vehicles were, the more difficult they became to sell. But generally, a very good month from the rostrum for our client stock.

Unless expressly stated to the contrary, the views expressed in this report are not necessarily the views of XBG or any of its subsidiaries or affiliates (Group Companies), and the Group Companies, their directors, officers and employees make no representations and accept no liability for its accuracy or completeness. This report, and any attachments are strictly confidential and intended for the addressee(s) only. The content may also contain legal, professional or other privileged information. If you are not the intended recipient, please notify the sender immediately and then delete the report. You should not disclose, copy or take any action in reliance on this transmission. You may report the matter by calling XBG Fleet Remarketing Ltd. You must ensure you have adequate virus protection before you open or detach any documents from or in this transmission. The Group Companies or XBG Fleet Remarketing Ltd do not accept any liability for viruses, howsoever caused or inflicted. An email reply to this address may be subject to monitoring for operational reasons or lawful business practices.