Wholesale Used Vehicle Market bucks seasonal trends

At this time of year as central heating thermostats start to click on and the nights draw in, the auction halls and online sales are generally less populated, and Trade interest wains considerably as Retail customers logically put off unnecessary purchases until the New Year. This year may be somewhat different in our wholesale world though. The shortage of stock in most sectors has created something of a clamour for all but the worst examples, even though Retail activity is not quite where the Trade would like it.

This surprisingly buoyant market has led to rising values with Guide prices increasing for the first time at this time of year for some years. While car value increases are fractional and not widespread, this is still a considerable change to what would normally be the state of play at this time of year.

In the LCV world the Guide value increases are widespread and even then, are somewhat behind the curve of what is actually happening in the auction halls.

Of course the looming Autumn Budget, and much talked about inevitable tax rises may well take the modest wind out of the sails of our economy, but the Used Vehicle Trade is enormously resilient, and with no large de-fleets expected now until the New Year we could well see a very unusual last quarter

Used LCV Market

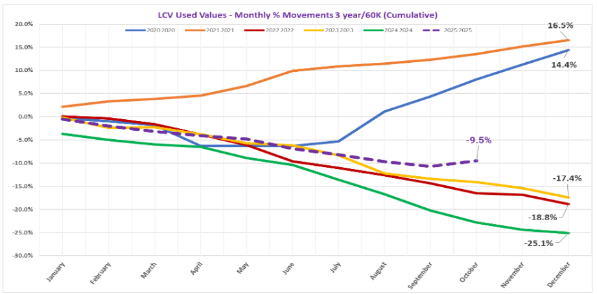

To illustrate just what is happening in the Used LCV wholesale market we’ve added this table courtesy of Cap-hpi, showing annual average value movements over the last few years. Ignoring the two pandemic years you can see the unusual nature of the dotted 2025 depreciation line showing not only a slower than average depreciation, but a remarkable uptick in values.

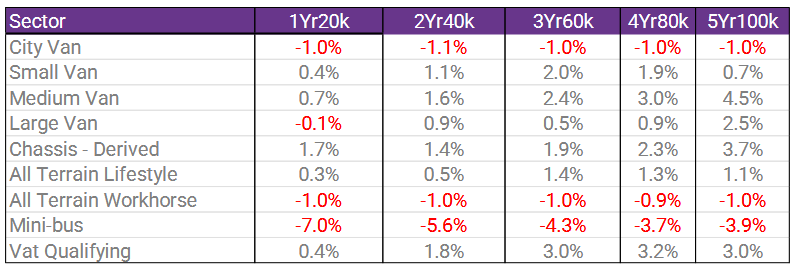

When examined more closely, looking at the sectoral and age/mileage splits, these wide-ranging value increases are even more remarkable, with the biggest increases being seen in the older lower price range vehicles.

At the time of writing the market continues to outperform Guide figures so we could see another rise in values next month.

It’s worth noting that the most commonly used and most reliable measurement of performance on Used Vehicle Wholesale is ‘% of CAP Average’ achieved, and this features across our Power BI reporting, so with CAP Average guide figures increasing month on month, the % of CAP Average reported will not reflect the whole story of how good the market is for the time of year.

If there is one area of concern in the LCV market it can only be in the Minibus world. This sector has suffered enormously over the last few months. Viewed in isolation they have seen the biggest roller coaster ride in values of virtually any vehicle type.

Following huge value reductions and lack of use in the pandemic the manufacturers stopped producing them completely in most instances. This then resulted in similarly huge post-pandemic used example price rises due to lack of availability of new stock.

That stock has now gradually come back into the used market with somewhat of a flurry in the last few months, with the buying trade realising that in many cases a brand-new version could be purchased more cheaply than the Guide value of a two year old one, thus resulting in the big value reductions now being seen.

So in summary, a bright picture across most of the LCV market to contrast the increasingly grey and damp images being captured as we continue to attend and actively promote our XBG auction sections across the country.

Used Car Market

While the Used Car Market is not as good as the LCVs, it is still in a good place for the time of year. We mentioned last month the widening gap between desirable and less-desirable models. Well, that seems to be less of a factor this month, with less stock available buyers are entertaining vehicles that they would have previously turned their noses up at.

Normally at this time of year main dealer Buyers will be absent from the auction halls as they manage their way out of September part-exchanges. But this year there is far more activity in this area, giving the independents and supermarkets a run for their money. Anecdotally, this is down to the ongoing success of the ‘car buying’ businesses, but with New Car sales slumping and manufacturers wrestling with ZEV Mandate targets it is more likely that less New Car deals were done involving retail ready part-exchanges.

The Used electric and Plug-in Hybrid car market continues to mature, with good levels of engagement from both Trade and Retail buyers now. Cars like this Polestar Long Range are now seen as solid reliable purchases that represent excellent value for money compared to ICE (petrol and diesel) cars of similar specification. Some Retailer statistics are even reporting that used BEV cars now sell in almost half the time of an ICE car when all makes and models are taken into account.

Trucks and Trailers

There was very little change in the truck and trailer markets again this month, although volumes of fresh stock entering the sales has fallen noticeably, by around 9% over the same period last year. This should be good news for pricing however, demand remains relatively flat so prices remain stable, but not up.

As with previous months, Boxes are around in quantity throughout the weight range and if anything, there are more standard Box trucks appearing at auction than any other type. As a consequence, unless they are very clean, low mileage or nearly new they are struggling to find buyers at anything like market price. But they do sell.

The same can be said for Dropsides which, although not available in volume, the demand is not really there either. If the truck is clean and low miles it will sell though and, usually first time out.

Rather interestingly, Manufacturers have reported a bumper sales month with the new registrations, which will serve to increase the annual registrations. This needed to happen because, thus far the volume of new truck registrations continues to be lower year on year, suggesting fewer used trucks coming back in the years to come.

This is happening particularly in the Tractor unit market, where lease deals from Manufacturers are so attractive that even small to medium size hauliers can avail themselves of new trucks, rather than used.

As a consequence, there are fewer (retail) used buyers out there, leading to many truck traders now only buying stock when they have orders; they no longer stock vehicles in the hope of a sale. So, for ex Supermarket stock such as that seen above in a Manheim sale this month, trying to sell in volumes is hard. These 4×2 Mercedes chassis are selling, but not in volume.

Older stock in the Box and Tractor unit sectors is now struggling to sell for anything other than parting out and scrap, which now also includes some early Euro 6 trucks.

The best performers this month are again small Tippers, larger Tippers with cranes, Hookloaders and Beavertail trucks, all of which are fairly rare at market and so sell for strong money.

Here was a truck that you don’t see every day, a 26-ton MAN 6×4 Hookloader chassis direct from the Fire Brigade, with less than 200000 miles recorded. It didn’t matter that this was over 10 years old, the immaculate condition and very low miles dictated a lot of strong interest and bidding with the sale price reaching £20000, easily beating the pre-sale estimate and reserve of £7000! This truck will undoubtedly assume a new identity as a tipper or horsebox before selling as a retail proposition.

The rather fragile state of the economy is also affecting used trailer sales, with just the newer stock being sold for further use. Older boxes and curtainsiders on 2 or 3 axles are really only useful now for parts or storage.

Of course, anything unusual, like nearly new trailers or specialist examples are still selling very well indeed to eager audiences.

Plant and Equipment

This month saw a lot of Excavators at all weight ranges coming to market; all are selling but dependant on their Manufacture, some more successfully than others.

Of particular concern are the Chinese machines, so Luigong or Sunwards which are beginning to appear quite frequently now. Whilst these machines do sell, they have to be cheap compared to their Western equivalents, often 50% cheaper or less. So, unless Vendors are realistic about pricing, the machines will simply sit and gather dust at auction. Realism is the name of this game.

Otherwise, plant and equipment is selling well still this month, with most stock gaining at least a bid at auction on which to work with.

From the Rostrum

Rostrum management continues to be the best way of achieving strong sale prices, with our managers acting on our client’s behalf to engage with the buyers. Many a deal is done during or after the sale at auction, especially if the asset does not reach the required price. Certainly, at the moment, buyers are reacting positively with rostrum presence, knowing that they can buy a vehicle rather than sit on a provisional bid.

As with previous month’s the view from our rostrum managers is that September and October have provided some excellent sales, with the trade being very active in selecting stock that they need.

Unless expressly stated to the contrary, the views expressed in this report are not necessarily the views of XBG or any of its subsidiaries or affiliates (Group Companies), and the Group Companies, their directors, officers and employees make no representations and accept no liability for its accuracy or completeness. This report, and any attachments are strictly confidential and intended for the addressee(s) only. The content may also contain legal, professional or other privileged information. If you are not the intended recipient, please notify the sender immediately and then delete the report. You should not disclose, copy or take any action in reliance on this transmission. You may report the matter by calling XBG Fleet Remarketing Ltd. You must ensure you have adequate virus protection before you open or detach any documents from or in this transmission. The Group Companies or XBG Fleet Remarketing Ltd do not accept any liability for viruses, howsoever caused or inflicted. An email reply to this address may be subject to monitoring for operational reasons or lawful business practices.