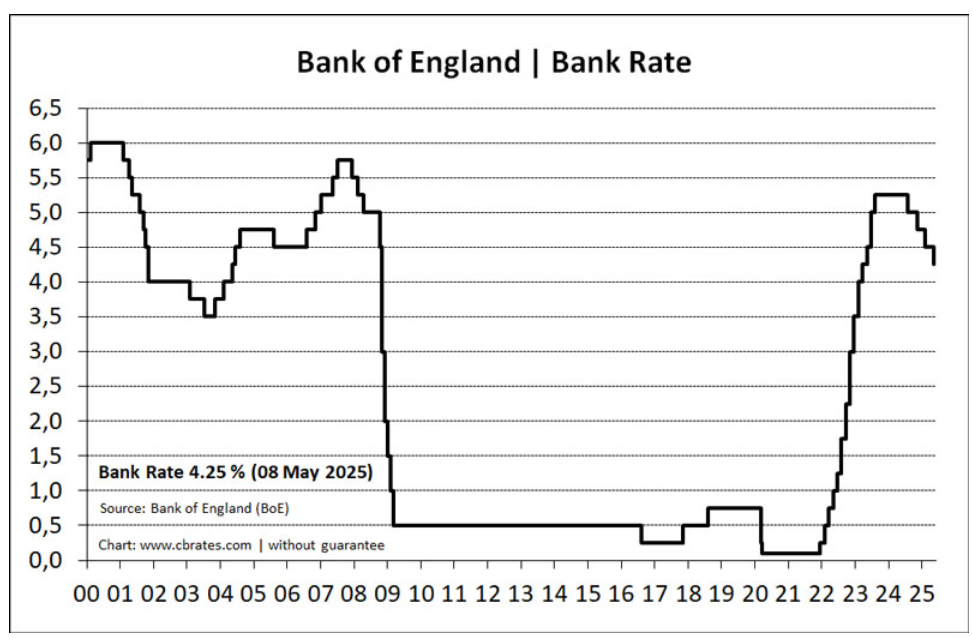

Amid the latest news that inflation is up and the number of unemployed in the UK has risen moderately, the Bank of England seems to be happy to allow the base interest rate to plateau at its current slightly uncomfortable level. Three years ago they predicted that late 2025 would probably be the point of near normalisation of interest rates, so if this is it, many mortgage payers, and businesses looking to borrow to invest will need to decide whether to lock in or wait for further reductions that may not now come.

This higher cost of borrowing when compared to decade long averages, combined with the much increased price of raw materials, and the increasing cost of labour due to inflation chasing pay settlements, Minimum Wage increases, and new NI rates, does nothing for the much lauded stimulation of UK business growth.

Add to this the unpredictable nature of international affairs and the overall health of the UK economy, and things do not bode well for future stability. So, it would seem that many businesses and consumers alike are now just ‘getting on with it’, while keeping one eye on contingency planning for worst case scenarios.

This very much the story of the current Used automotive sector, and the second-hand machinery and plant business too. There is no doubt that business is harder and that profit margins are substantially reduced from those enjoyed during the 2010s, but there is safety in doing what you know, and most dealers seem happy to plough on, passing as many of their increased costs onto the embattled customer as commerciality will allow.

LCV Market

While the early part of the year saw an increase of over 20% in Used van stock around the auctions, around 1 in 5 were still making over their CAP guide values. Since April volumes have dropped back across all vendor sectors, so understandably prices achieved have remained quite strong, with guide valuations moving down much more slowly than would normally be expected.

The average age of vans sold in auction remains between 6 and 7 years, with mileages of circa 80k. Interestingly only 15% of vehicles offered for sale were under 60k in mileage, making low mileage examples rare, and skewing the relative values for these upwards.

The average value of a van sold in auction was approximately £8000 when this was last measured in May, but it should be remembered that the skewing of later year, low mileage values pulls this figure up to somewhat more than might be estimated.

There is however a large influx (approx. 2500 units) of ex rental stock from one business just hitting the auctions. And although the volume in itself isn’t hugely significant, the narrow window given to sell it, and the repetitive nature of the models offered, is just starting to affect prices negatively in some sectors. Hopefully these will wash through quickly without pulling the rest of the market down too much.

The Holy Grail of good auction business is of course sale Conversion Rates, and these are still in excess of 70% in most businesses, meaning that ongoing costs incurred storing and rerunning sales are kept to a minimum.

Our XBG sale sections continue to be incredibly popular with the Trade, and it’s great to be representing our clients and the XBG business at auction when you are approached by eager Buyers wanting to know when certain vehicles will next be offered for sale!

So, in summing up, the established LCV market remains resilient, and largely in a good place, with the outlook for the latter part of the year showing no signs of immediate change.

Car Market

As mentioned last month the wholesale car market is much more of a challenge, and with auction stocks at quite high levels, there is plenty for the Trade to choose from. And what a choice!

Statistically, and in stark contrast to the LCV world, BEV Cars are amongst the fastest moving in the Retail market due to their ‘value for money’ against cost new, and reduced running costs for some domestic users. While in some rural areas there is still an overwhelming demand for Diesel variants, and in other areas petrol is the most sought after.

Add to this the news that Plug-in Hybrids are some of the best Retail sellers amongst new vehicles and the picture of what to stock as a Used car gets quite confusing for less than experienced dealers.

At the risk of stating the obvious though, ultimate Used Car desirability still revolves around prestigious but accessible brands, with high specifications, and good pedigree in terms of service history and a low number of owners.

While values are stabilising a little from the reductions we saw in May and June, many ‘ordinary’ models align more closely with CAP Average and Below guide figures, than with CAP Clean values.

Trucks and Trailers

The only changes to the truck markets this month have been a distinct lack of stock entering the arena, which has further strengthened prices across the board. There does remain some nervousness amongst buyers about prices increasing as a result of this lack of supply because, the moment supply turns on again such high stock prices would become unattainable, hence the conservative nature of bidding currently on standard stock.

In the light 7.5 ton box markets, stock levels remain stable with a few fresh entries arriving each week. However, sales are also very good, especially for the cleaner lower mileage examples which sell on their first outing. Even the red box trucks are selling, as the vendor remains realistic over pricing.

In the heavier box sector, the news is much the same, except that at 16-18 tons a standard box without fridge or sleeper cab can struggle a little, with not a lot of retail demand for such basic trucks. If that truck is also on a DAF, Renault or Iveco chassis then it will struggle to find a new home.

Tractor units are still selling because here again, volumes remain low. Thus, low spec, day cab small engine 4×2’s such as the ex-supermarket Scania seen below are selling and making relatively good money. Any amount of volume into this basic sector will immediately affect pricing though.

Fully specified 6×2 tractors with sleepers are much better news and all find new homes relatively easily this month. Of course, a 6×4 example needs no help whatsoever at market and will easily sell for more than any pre-sale estimates, such is their rarity.

Specialist trucks continue to sell well, even older examples like this DAF flat with a crane fitted will make strong money. Being Euro 6 helps enormously but, to be honest there are not that many pre-Euro 6 trucks now at market.

Trailer sales also remain stable this month owing to a lack of volume. The best money is always reserved for the more specialist trailers, such as this low loader seen at market this month. Curtainsiders and Boxes are selling, with the newer ones commanding the best money. Any significant increase in volume could quickly turn this market back into difficult times though, as many of the trade are fully aware.

Plant and Equipment

The plant and equipment markets remain the same this month, very strong!

Even smaller sales such as the CVA offering seen above this month command very strong prices, because the export markets remain extremely active currently.

Perhaps one area that is suffering is the ‘winter dependent’ items, such as snow ploughs. As most of the UK and Europe bakes in unprecedented temperatures (according to the media!) there is little appetite to buy snow ploughs and the like. The canny buyers are there though, because they know that it will not be long before everyone wants a plough so, to buy very cheaply now and store for a few months is not really a problem!

From the Rostrum

With such buoyant markets currently, rostrum management can be quite frenetic, trying to capture the real bids from those that are not. Our very experienced Auction Managers are very adept at this and very often spot proper bids that the auctioneers have missed, in a busy sale room.

Yet again this month, many car sales are converted from the rostrum after the bidding has finished in the auction room, with a provisional bidder asking our Managers how much as asset must be. The deal is very often done there and then, proving the need for attendance at every sale. This is particularly true this month in the used car markets, where life is a bit tough created by a lack of retail demand.

Traders are only really buying the nicer cars or, those where they need to replenish the forecourt. In either case the trade are looking to pay as little as possible to own the stock, such is their nervousness of holding stock for longer than usual.

Unless expressly stated to the contrary, the views expressed in this report are not necessarily the views of XBG or any of its subsidiaries or affiliates (Group Companies), and the Group Companies, their directors, officers and employees make no representations and accept no liability for its accuracy or completeness. This report, and any attachments are strictly confidential and intended for the addressee(s) only. The content may also contain legal, professional or other privileged information. If you are not the intended recipient, please notify the sender immediately and then delete the report. You should not disclose, copy or take any action in reliance on this transmission. You may report the matter by calling XBG Fleet Remarketing Ltd. You must ensure you have adequate virus protection before you open or detach any documents from or in this transmission. The Group Companies or XBG Fleet Remarketing Ltd do not accept any liability for viruses, howsoever caused or inflicted. An email reply to this address may be subject to monitoring for operational reasons or lawful business practices.